Posted: 15 Sep 2016 Michael Snyder THE ECONOMIC COLLAPSE BLOG

Can Donald Trump turn the U.S. economy around? This week Trump unveiled details of his new economic plan, and the mainstream media is having a field day criticizing it. But the truth is that we simply cannot afford to stay on the same path that Barack Obama, Hillary Clinton and the Democrats have us on right now.

Millions of jobs are being shipped out of the country, the middle class is dying, poverty is exploding, millions of children in America don’t have enough food, and our reckless spending has created the biggest debt bubble in the history of the planet. Something must be done or else we will continue to steamroll toward economic oblivion. So is Donald Trump the man for the hour?

If you would like to read his full economic plan, you can find it on his official campaign website. His plan starts off by pointing out that this has been the weakest “economic recovery” since the Great Depression…

So how would he fix things?

The following are 10 things that every American should know about Donald Trump’s plan to save the U.S. economy…

#1 Donald Trump would lower taxes on the middle class

The tax savings under Trump’s plan would actually be quite substantial for middle class families. The following numbers come from a recent Charisma article…

• A married couple earning $50,000 per year with two children and $8,000 in child care expenses will save 35% from their current tax bill.

• A married couple earning $75,000 per year with two children and $10,000 in child care expenses will receive a 30% reduction in their tax bill.

• Married couple earning $5 million per year with two children and $12,000 in child care expenses will get only a 3% reduction in their tax bill.

#2 Donald Trump would lower taxes on businesses

Under his plan, no business in America would be taxed more than 15 percent. Alternatively, Hillary Clinton’s plan would tax some small businesses at a rate of close to 50 percent. So Trump’s plan would undoubtedly be good for businesses, and it would encourage many that have left the country to return.

But where would the lost tax revenue be made up?

#3 Childcare expenses would be exempt from taxation

For working families with children this would be a great blessing. Without a doubt this is an effort to win over more working women, and this is a demographic that Trump has been struggling with.

It is definitely an idea that I support, but once again where will the money come from to pay for this?

#4 U.S. manufacturers will be allowed to immediately fully expense new plants and equipment

This would undoubtedly lead to a boom in capital investment, but it would also reduce tax revenue. As an emergency measure this would be very good for encouraging manufacturers to stay in America, but it would also likely increase the budget deficit.

#5 A temporary freeze on new regulations

Red tape is one of my big pet peeves, and so I greatly applaud Trump for this proposal. I think that Bob Eschliman put it very well when he wrote the following about Trump’s planned freeze on new regulations…

In particular, Trump’s plan would focus on getting rid of regulations that inhibit hiring. The following are some of the specific areas that he identifies on his official campaign website…

Donald Trump is the first major party nominee in decades to recognize that our trade deficit is absolutely killing our economy. I write about this all the time, and it is a hot button issue for me. So I definitely applaud Trump for proposing the following…

Barack Obama promised to kill the coal industry, and that is one of the few promises that he has actually kept. Obama also killed the Keystone Pipeline, and right now the energy industry as a whole is enduring their worst stretch since the last recession. To turn things around, Trump would do the following…

Trump claims that Obamacare would cost our economy two million jobs over the next ten years. And without a doubt, it has already cost the U.S. economy a lot of jobs. Not only that, but Obamacare has also sent health insurance premiums soaring, and this is putting a tremendous amount of financial pressure on many families.

Trump says that he would “replace” Obamacare, but that is a rather vague statement.

What exactly would he replace it with?

#10 Trump’s plan says nothing about the Federal Reserve

This is a great concern, because the Federal Reserve has far more power over the economy than anyone else does. It is at the very heart of our debt-based system, and unless something is done about the Fed our debt bubble will continue to get even larger.

Since the Federal Reserve was created in 1913, the value of the U.S. dollar has fallen by more than 96 percent and our national debt has gotten more than 5000 times larger. For Trump to not even mention the Federal Reserve in his economic plan is a tremendous oversight.

We are in the midst of a long-term economic decline, and things have not gotten better during the Obama years. If you can believe it, a study that was just released by Harvard even acknowledges this…

If we continue to do the same things, we will continue to get the same results.

Donald Trump is promising change, and many of his proposals sound good, but there are also some areas to be concerned about.

Ultimately, just tinkering with the tax code and reducing regulations is not going to be enough to turn the U.S. economy around. We need a fundamental overhaul of our economic and financial systems, and Trump’s plan stops well short of that. But without a doubt what he is proposing is vastly superior to Hillary Clinton’s plan, and so he should definitely be applauded for at least moving in the right direction.

Millions of jobs are being shipped out of the country, the middle class is dying, poverty is exploding, millions of children in America don’t have enough food, and our reckless spending has created the biggest debt bubble in the history of the planet. Something must be done or else we will continue to steamroll toward economic oblivion. So is Donald Trump the man for the hour?

If you would like to read his full economic plan, you can find it on his official campaign website. His plan starts off by pointing out that this has been the weakest “economic recovery” since the Great Depression…

Last week’s GDP report showed that the economy grew a mere 1.2% in the second quarter and 1.2% over the last year. It’s the weakest recovery since the Great Depression – the predictable consequence of massive taxation, regulation, one-side trade deals and onerous energy restrictions.And Trump is exactly right about how weak this economic recovery has been.

So how would he fix things?

The following are 10 things that every American should know about Donald Trump’s plan to save the U.S. economy…

#1 Donald Trump would lower taxes on the middle class

The tax savings under Trump’s plan would actually be quite substantial for middle class families. The following numbers come from a recent Charisma article…

• A married couple earning $50,000 per year with two children and $8,000 in child care expenses will save 35% from their current tax bill.

• A married couple earning $75,000 per year with two children and $10,000 in child care expenses will receive a 30% reduction in their tax bill.

• Married couple earning $5 million per year with two children and $12,000 in child care expenses will get only a 3% reduction in their tax bill.

#2 Donald Trump would lower taxes on businesses

Under his plan, no business in America would be taxed more than 15 percent. Alternatively, Hillary Clinton’s plan would tax some small businesses at a rate of close to 50 percent. So Trump’s plan would undoubtedly be good for businesses, and it would encourage many that have left the country to return.

But where would the lost tax revenue be made up?

#3 Childcare expenses would be exempt from taxation

For working families with children this would be a great blessing. Without a doubt this is an effort to win over more working women, and this is a demographic that Trump has been struggling with.

It is definitely an idea that I support, but once again where will the money come from to pay for this?

#4 U.S. manufacturers will be allowed to immediately fully expense new plants and equipment

This would undoubtedly lead to a boom in capital investment, but it would also reduce tax revenue. As an emergency measure this would be very good for encouraging manufacturers to stay in America, but it would also likely increase the budget deficit.

#5 A temporary freeze on new regulations

Red tape is one of my big pet peeves, and so I greatly applaud Trump for this proposal. I think that Bob Eschliman put it very well when he wrote the following about Trump’s planned freeze on new regulations…

In 2015 alone, federal agencies issued over 3,300 final rules and regulations, up from 2,400 the prior year. Studies show that small manufacturers face more than three times the burden of the average U.S. business, and the hidden tax from ineffective regulations amounts to “nearly $15,000 per U.S. household” annually. Excessive regulation is costing our country as much as $2 trillion dollars per year, and Trump will end it.#6 All existing regulations would be reviewed and unnecessary regulations would be eliminated

In particular, Trump’s plan would focus on getting rid of regulations that inhibit hiring. The following are some of the specific areas that he identifies on his official campaign website…

- The Environmental Protection Agency’s Clean Power Plan, which forces investment in renewable energy at the expense of coal and natural gas, raising electricity rates;

- The EPA’s Waters of the United States rule, which gives the EPA the ability to regulate the smallest streams on private land, limiting land use; and

- The Department of Interior’s moratorium on coal mining permits, which put tens of thousands of coal miners out of work.

Donald Trump is the first major party nominee in decades to recognize that our trade deficit is absolutely killing our economy. I write about this all the time, and it is a hot button issue for me. So I definitely applaud Trump for proposing the following…

- Appoint trade negotiators whose goal will be to win for America: narrowing our trade deficit, increasing domestic production, and getting a fair deal for our workers.

- Renegotiate NAFTA.

- Withdraw from the TPP.

- Bring trade relief cases to the world trade organization.

- Label China a currency manipulator.

- Apply tariffs and duties to countries that cheat.

- Direct the Commerce Department to use all legal tools to respond to trade violations.

Barack Obama promised to kill the coal industry, and that is one of the few promises that he has actually kept. Obama also killed the Keystone Pipeline, and right now the energy industry as a whole is enduring their worst stretch since the last recession. To turn things around, Trump would do the following…

- Rescind all the job-destroying Obama executive actions including the Climate Action Plan and the Waters of the U.S. rule.

- Save the coal industry and other industries threatened by Hillary Clinton’s extremist agenda.

- Ask Trans Canada to renew its permit application for the Keystone Pipeline.

- Make land in the Outer Continental Shelf available to produce oil and natural gas.

- Cancel the Paris Climate Agreement (limit global warming to 2 degrees Celsius) and stop all payments of U.S. tax dollars to U.N. global warming programs.

Trump claims that Obamacare would cost our economy two million jobs over the next ten years. And without a doubt, it has already cost the U.S. economy a lot of jobs. Not only that, but Obamacare has also sent health insurance premiums soaring, and this is putting a tremendous amount of financial pressure on many families.

Trump says that he would “replace” Obamacare, but that is a rather vague statement.

What exactly would he replace it with?

#10 Trump’s plan says nothing about the Federal Reserve

This is a great concern, because the Federal Reserve has far more power over the economy than anyone else does. It is at the very heart of our debt-based system, and unless something is done about the Fed our debt bubble will continue to get even larger.

Since the Federal Reserve was created in 1913, the value of the U.S. dollar has fallen by more than 96 percent and our national debt has gotten more than 5000 times larger. For Trump to not even mention the Federal Reserve in his economic plan is a tremendous oversight.

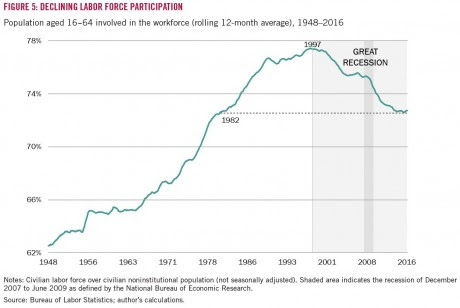

We are in the midst of a long-term economic decline, and things have not gotten better during the Obama years. If you can believe it, a study that was just released by Harvard even acknowledges this…

America’s economic performance peaked in the late 1990s, and erosion in crucial economic indicators such as the rate of economic growth, productivity growth, job growth, and investment began well before the Great Recession.That same study found that the percentage of Americans participating in the labor force peaked back in 1997 and has been steadily declining since that time…

Workforce participation, the proportion of Americans in the productive workforce, peaked in 1997. With fewer working-age men and women in the workforce, per-capita income for the U.S. is reduced.

Median real household income has declined since 1999, with incomes stagnating across virtually all income levels. Despite a welcome jump in 2015, median household income remains below the peak attained in 1999, 17 years ago. Moreover, stagnating income and limited job prospects have disproportionately affected lower-income and lower-skilled Americans, leading inequality to rise.

Donald Trump is promising change, and many of his proposals sound good, but there are also some areas to be concerned about.

Ultimately, just tinkering with the tax code and reducing regulations is not going to be enough to turn the U.S. economy around. We need a fundamental overhaul of our economic and financial systems, and Trump’s plan stops well short of that. But without a doubt what he is proposing is vastly superior to Hillary Clinton’s plan, and so he should definitely be applauded for at least moving in the right direction.